As I reflect on my own financial journey, I can’t help but wonder how many others out there find themselves grappling with the same question: Am I on track with my retirement savings? It’s a common concern that keeps many individuals up at night, worried about the uncertainty of their golden years.

But what if I told you that there’s a tool that can help guide you towards a secure and comfortable retirement? Enter the retirement savings by age chart – a powerful resource that can illuminate the path forward, no matter your current stage in life.

In my experience, understanding these benchmarks has been a game-changer. It’s allowed me to set realistic goals, make informed decisions, and take control of my financial future. And I’m excited to share this knowledge with you, so you can embark on your own journey towards a worry-free retirement.

Understanding the Retirement Savings Landscape

The retirement savings landscape can be a complex and daunting one, with a myriad of factors to consider. But don’t worry, we’re here to break it down into manageable pieces.

First and foremost, it’s important to understand the concept of retirement savings benchmarks. These guidelines, provided by reputable financial institutions like Fidelity, offer a roadmap for how much you should have saved at various stages of your life.

While these benchmarks are not one-size-fits-all, they can serve as a valuable starting point for your retirement planning. According to Fidelity, the recommended target is to have 10 times your pre-retirement income saved by age 67.

To help you stay on track, they suggest aiming for the following retirement savings milestones:

- Age 30: At least 1 times your current income

- Age 40: 3 times your current income

- Age 50: 6 times your current income

- Age 60: 8 times your current income

Of course, your personal savings goals may vary based on factors like your desired retirement age, lifestyle expectations, and other financial obligations. But these benchmarks provide a solid foundation to build upon.

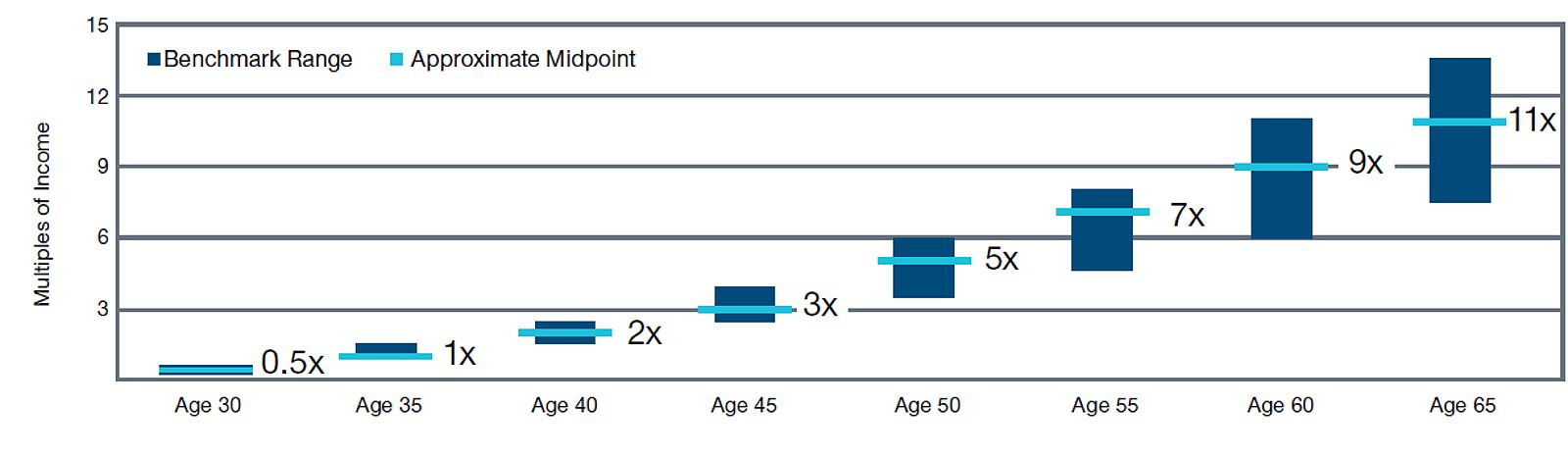

Retirement Savings by Age Chart: Visualizing Your Journey

Now that we’ve established the importance of retirement savings benchmarks, let’s take a closer look at a retirement savings by age chart:

| Age | Savings Target (as a multiple of income) |

|---|---|

| 30 | 1x – 1.5x |

| 35 | 1.5x – 2.5x |

| 40 | 2.5x – 4x |

| 45 | 3.5x – 6x |

| 50 | 4.5x – 8x |

| 55 | 6x – 11x |

| 60 | 7.5x – 13.5x |

This chart offers a range of savings targets based on your current income level, with the lower end of the range catering to those with lower incomes and the higher end geared towards higher earners.

As you review this chart, I encourage you to reflect on your own financial situation and where you fall within these benchmarks. Are you on track, or do you find yourself playing catch-up? Regardless of your current position, this chart can serve as a valuable tool to help you navigate the path ahead.

Building a Strong Foundation: Retirement Savings by Age 35

One of the key lessons I’ve learned on my own financial journey is the importance of starting early. When it comes to retirement savings, time is truly on your side, and the earlier you begin, the more you can harness the power of compounding.

By the time you reach age 35, you should aim to have saved the equivalent of one to one-and-a-half times your current income. I know, it might sound like a lofty goal, but trust me, it’s achievable with a consistent and strategic approach.

Some of the strategies that have worked well for me include:

- Maximizing my employer-sponsored retirement accounts, especially if there’s a matching contribution.

- Automating my savings by setting up recurring transfers from my paycheck to my retirement accounts.

- Gradually increasing my savings rate over time, with the goal of saving at least 15% of my income for retirement.

Remember, every little bit counts when it comes to building a solid financial foundation. The earlier you start, the less you’ll need to contribute each year to reach your retirement goals.

Mid-Career Milestones: Retirement Savings by Age 45

As you reach your mid-40s, it’s important to take a step back and assess your retirement savings progress. By this age, you should have accumulated savings equivalent to three-and-a-half to six times your current income.

If you find yourself falling behind on your savings goals, don’t be discouraged. There are several strategies you can employ to catch up:

- Increase your retirement contributions, even if it’s just a small amount. Every dollar makes a difference.

- Explore opportunities to earn extra income through a side gig or freelance work, and dedicate those funds towards your retirement savings.

- Review your expenses and identify areas where you can cut back, freeing up more money to allocate towards your retirement accounts.

- Consider delaying your retirement by a few years, which can significantly boost your savings and provide a higher Social Security benefit.

Remember, it’s never too late to start saving for retirement. With a focused and persistent approach, you can get back on track and secure your financial future.

Catching Up on Retirement Savings: Strategies for Success

I know firsthand that life can throw unexpected curveballs, making it difficult to stay on top of your retirement savings. But the good news is, there are always strategies you can employ to catch up.

One of the most effective ways to do this is to increase your savings rate. This might mean making some tough decisions, like cutting back on unnecessary expenses or finding ways to boost your income, such as taking on a side job or negotiating a higher salary.

Another option to consider is delaying your retirement. By working for a few more years, you can continue to contribute to your retirement accounts and allow your savings to grow. This can also increase your Social Security benefits, providing you with a larger income stream in retirement.

If you’re nearing retirement age and still haven’t saved enough, you may need to adjust your expectations and lifestyle. This could involve downsizing your home, relocating to a more affordable area, or finding ways to reduce your overall expenses.

Remember, it’s never too late to start saving for retirement. With a well-crafted plan and a commitment to making it a priority, you can overcome any savings shortfall and enjoy a comfortable and financially secure retirement.

Retirement Planning: Beyond the Savings Chart

While the retirement savings by age chart is a valuable tool for setting and tracking your financial goals, it’s important to consider other aspects of retirement planning as well.

In addition to building up your retirement savings, you’ll need to think about your income sources in retirement, such as Social Security benefits, pensions, and any other investments or assets you may have. It’s also crucial to plan for healthcare expenses, long-term care needs, and estate planning.

To ensure you have a comprehensive retirement plan, I highly recommend seeking the guidance of a financial advisor. They can help you assess your current financial situation, develop a customized retirement strategy, and provide ongoing support as you navigate the various stages of retirement.

FAQ

Q: What if I don’t have a 401(k) at work?

A: If you don’t have access to a 401(k) through your employer, you can still save for retirement through an individual retirement account (IRA). Both traditional IRAs and Roth IRAs offer tax-advantaged savings opportunities, so be sure to explore your options and choose the one that best fits your financial situation.

Q: How much should I save each year for retirement?

A: As a general rule of thumb, it’s recommended to aim to save 15% of your gross income each year for retirement. However, this can vary depending on your age, income, and retirement goals. It’s best to consult with a financial advisor to determine the appropriate savings rate for your unique circumstances.

Q: What if I’m already retired, but I haven’t saved enough?

A: If you’re already retired and haven’t saved enough, there are still options available to you. You can consider working part-time, delaying your full retirement, or adjusting your lifestyle to reduce expenses. It’s important to seek professional advice to explore your options and develop a plan to address your financial situation.

Conclusion

As I reflect on my own journey, I’m reminded of the power of financial empowerment. The retirement savings by age chart has been an invaluable tool in helping me take control of my financial future, and I’m confident it can do the same for you.

Whether you’re just starting out, in the middle of your career, or nearing retirement, this chart can serve as a roadmap to guide you towards a secure and comfortable retirement. By understanding the benchmarks, developing a personalized plan, and seeking professional guidance, you can overcome any savings challenges and enjoy the peace of mind that comes with financial stability.

So, take the first step today. Evaluate your current savings, set realistic goals, and commit to making your retirement a top priority. With a focused and persistent approach, you can build the financial future you deserve.